Are You a Victim?

Housing Discrimination

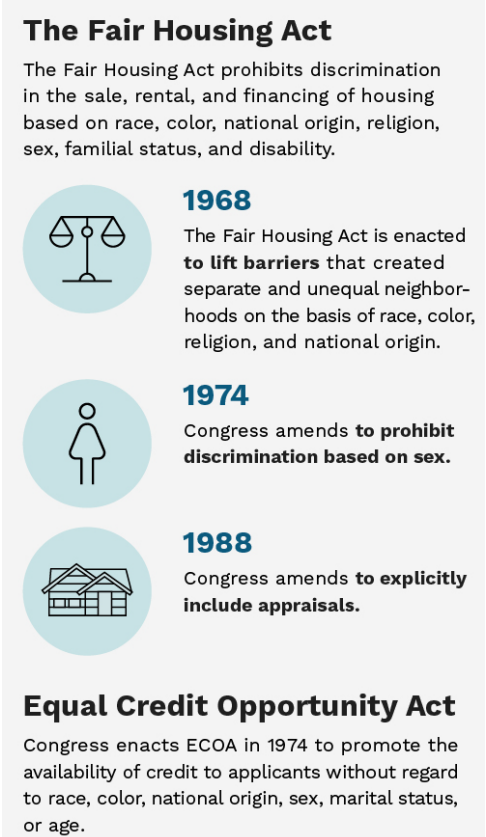

Laws prohibit racial and other discrimination in housing. Yet housing experts and civil rights attorneys say bias remains persistently challenging to prove, let alone eliminate. Here’s how to recognize housing discrimination, the laws that are meant to protect you from it, and how to fight it.

Fair Housing Act Prohibits Discrimination in Appraisals

On February 14, 2022, DOJ filed a statement of interest to make clear that the Fair Housing Act prohibits discrimination in home appraisals. The statement relates to a motion to dismiss filed in Austin, et al. v. Miller, et al. (N.D. Cal.), a private lawsuit alleging that the defendants violated the Fair Housing Act by discriminating on the basis of race in a home appraisal. After the defendants’ appraisal, the plaintiffs — a Black couple — erased all evidence of race from their home and had a white friend pose as the homeowner for a second appraisal, which set the home’s value at nearly $500,000 more. The statement of interest explains that appraisers may be liable under the Fair Housing Act, highlights the United States’ commitment to combat appraisal discrimination, provides an overview of the Fair Housing Act’s broad purpose and remedial intent, and addresses the pleading standard for Fair Housing Act claims.

What is a Reconsideration of Value (ROV)

A reconsideration of value (ROV) may be requested by consumers to reassess the analysis and conclusions of their initial appraisal when provided with additional information that may affect the value conclusion. Consumers can provide information to a lender during an ROV request that includes additional comparable property information and additional information pertaining to characteristics of the subject property, such as square footage. An ROV offers consumers who suspect that their appraisal may have been influenced by racial or ethnic bias an avenue by which they might be able to request a different valuation that results in a better outcome.

We Offer:

-

![Remove Barriers of Entry]()

Remove Barriers of Entry

ButtonBarriers of entry is an economic and business term describing factors that can prevent or impede newcomers in a market or industry sector and limit competition. These can include finding a supervisory appraiser, low starting pays, and other obstacles. That prevents minorities and women from entering the field and creating generational wealth for themselves and their families. We have found some solutions to this issue.

Remove Barriers of Entry

Request

A Free Consultation

Submit your request, and we'll get back to you soon.

UCAP is connected with several national organization including;

- Nation Community Reinvestment Coalition (NCRC)

- Greater Cincinnati Community Reinvestment Coalition (GCCRC)

- The Appraisal Foundation

- National Housing Alliance (NFHA)

- National Appraisal Bias Taskforce (NABT)

- National Association for the Advancement of Colored People (NAACP)

- Housing Opportunities Made Equal (HOME)

- The Urban Coalition of Appraisal Professionals was added to The Appraisal Foundation Advisory Council (TAFAC)